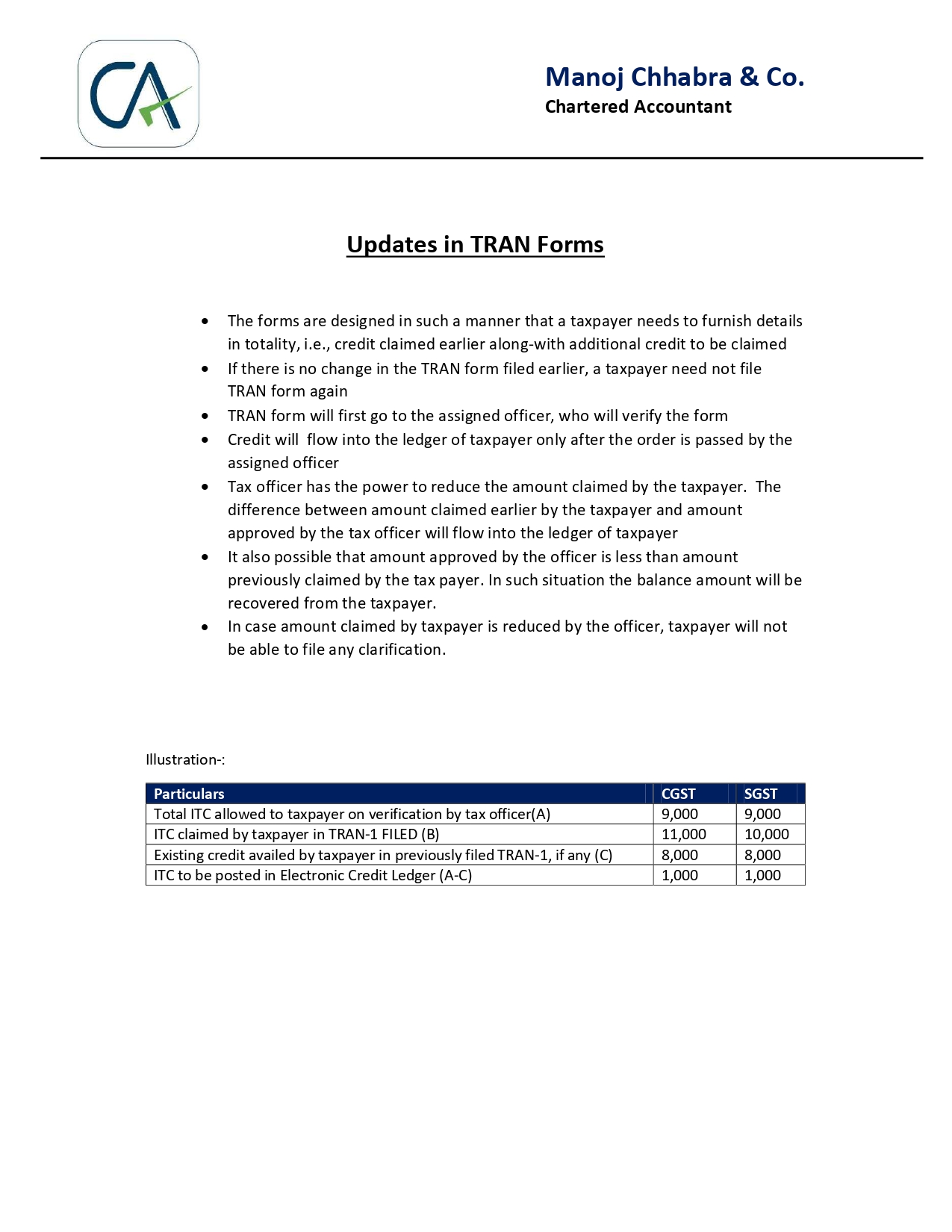

Key Highlights of Budget 2023- Direct Tax

01 Feb 20231) Changes in tax rates from AY 2024-25

W.e.f. AY 2024-25, the tax slabs under new regime (section 115BAC) have been revised as follows:

|

Sr. No |

Income |

Tax Rate |

|

1 |

Upto Rs 3 lakhs |

Nil |

|

2 |

From Rs. 3,00,001 to Rs. 6,00,000 |

5% |

|

3 |

From Rs. 6,00,001 to Rs.9,00,000 |

10% |

|

4 |

From Rs. 9,00,001 to Rs. 12,00,000 |

15% |

|

5 |

From Rs. 12,00,001 to Rs. 15,00,000 |

20% |

|

6 |

Above Rs. 15,00,000 |

30% |

The above rates would be mandatorily applicable to all individual or Hindu undivided family or association of persons [other than a co-operative society], or body of individuals, whether incorporated or not, or an artificial juridical person referred to in sub-clause (vii) of clause (31) of section 2, unless an option is exercised under proposed sub-section (6) of section 115BAC.

Earlier, no deductions were allowed under new regime of taxation u/s 115BAC. From AY 2024-25, the following deductions will be allowed-

If persons having income from business or profession exercise the option to opt out (by filing the relevant form) in a particular AY, then such option will continue to subsequent AYs and they will have only 1 opportunity to opt back.

Others can opt in or out every year. No form is needed to be filed by such persons and option to be exercised at the time of filing of ITR for each AY.

Surcharge @ 37% has been reduced to 25%, ie, surcharge on income above 2 crores is now 25% for those not opting out from new regime.

Further, rebate u/s 87A is extended to individuals not opting out of section 115BAC if the total income is upto Rs 7 lakhs.

2) Payments to MSMEs included u/s 43B from AY 2024-25

It has been proposed that expenses related to micro or small vendors as per MSMED Act will be allowed only on payment basis, ie, if payment is not made to such vendors within 45 days, expense can be claimed only if payment has been made before the due date of filing of return.

3) Relief to start-ups in carry forward and set off of losses from AY 2023-24

The benefit of losses incurred upto 7 years from the formation of company has been extended to 10 years u/s 79.

4) Extension of date of incorporation for eligible start-up for exemption

The benefit of section 80-IAC has been extended to start-ups incorporated in FY 2023-24.

5) Increase in threshold for presumptive taxation scheme from AY 2024-25

The turnover limits for presumptive taxation have been increased from Rs 2 crores to Rs 3 crores for businesses u/s 44AD and Rs 75 lakhs for professions u/s 44ADA provided receipts in cash do not exceed 5% of the turnover.

6) Gifts to NORs have been made taxable in India from AY 2024-25 by proposing amendments u/s 9.

7) Increase in TCS rates from July 01, 2023

TCS rate has been increased from 5% to 20% on overseas tour packages.

8) Limits on benefits u/s 54 and 54F from AY 2024-25

A ceiling of Rs 10 crores has been imposed on deductions u/s 54 and 54F.

9) Valuation of Inventory from cost accountant from AY 2023-24

The AO is now enabled to direct the assessees to get their inventory valued by cost accountants during assessment proceedings.

10) Taxability of Insurance Proceeds on policies issued on or after April 01, 2023

Maturity claims on new insurance policies (other than ULIPs) issued on or after April 01, 2023 where annual premium exceeds Rs 5 lakhs (in aggregate for all policies issued after April 01, 2023) has been made taxable. However, if receipts are on account of death of the insured person, they continue to be exempt.

11) Prevention of double deduction of interest expense related to house property from AY 2024-25

It has been proposed that interest expense, if claimed as deduction u/s 24 or chapter VI-A will not be allowed again as deduction in the form of cost of acquisition or cost of improvement when such property is sold.

12) TDS credit for income reported in a year but TDS deducted by deductor in next year(s)

Now, an assessee can make an application before the concerned AO within 2 years from the end of FY in which such tax was deducted to get the benefit of such TDS.

13) Taxation of security premium received from non-resident investors from AY 2024-25

To bring non-resident investors at par with resident investors, the provisions of section 56(2)(viib) have been made applicable on non-residents as well.

14) Non deduction of expenses out of corpus by charitable organisations from AY 2023-24

Amendments have been made to ensure expenses out of corpus are not claimed by charitable organisations.

15) Restriction on expense claims by charitable organisations if they further make donations to other charitable organisations from AY 2024-25

It has been proposed that only 85% of donations made by a charitable organization to another organization will be treated as application of income for charitable purposes.

16) Cancellation of registration granted to trusts

It has been proposed to cancel registration of trusts in cases where the system granted them automatic registration but the application filed for such registration was not correct.

17) Change in timelines for filing form 9A/10 by charitable organisations from AY 2023-24

These forms were earlier required to be filed before the due date of filing of return. It is proposed to reduce the timeline from due date of return to two months before the due date of filing of return.

18) Removal of certain funds from section 80G from AY 2024-25

The benefit of 50% deduction to various funds, namely Jawaharlal Nehru Memorial Fund, Indira Gandhi Memorial Trust and Rajiv Gandhi Foundation is proposed to be discontinued.

Manoj Chhabra & Co. is a Delhi-based accounting, auditing, tax and management consultancy firm. It was established in 1995. Since its foundation, its growth has been continuous and accelerated in recent years.

316, Vikas Surya plaza, sector-3, Rohini, Delhi-110085

+91-9871735391

info@mchhabra.com

Copyright © 2022 Mc Chhabra. All rights reserved. | Designed & Developed by : Global Ad Media